Every good you buy and every service you use exists because someone combined resources in a specific way. A cup of tea, a mobile app, a hospital service, a bus ride, a pair of shoes, a wheat harvest, a movie, even a haircut, all of them are the result of production. And production, in economics, starts with one core question: what are the factors of production?

In simple terms, factors of production are the inputs used to produce goods and services. They are the building blocks of an economy. When businesses decide what to produce, how much to produce, and how to produce, they’re really deciding how to use these factors in the smartest possible way.

This article will explain the factors of production in depth, with examples, real-life relevance, and the economic logic behind them. You’ll also see why the concept of factors of production in economics is not just theory, it’s a practical framework that explains wages, profits, growth, and even inequality.

What Are the Factors of Production?

What are the factors of production?

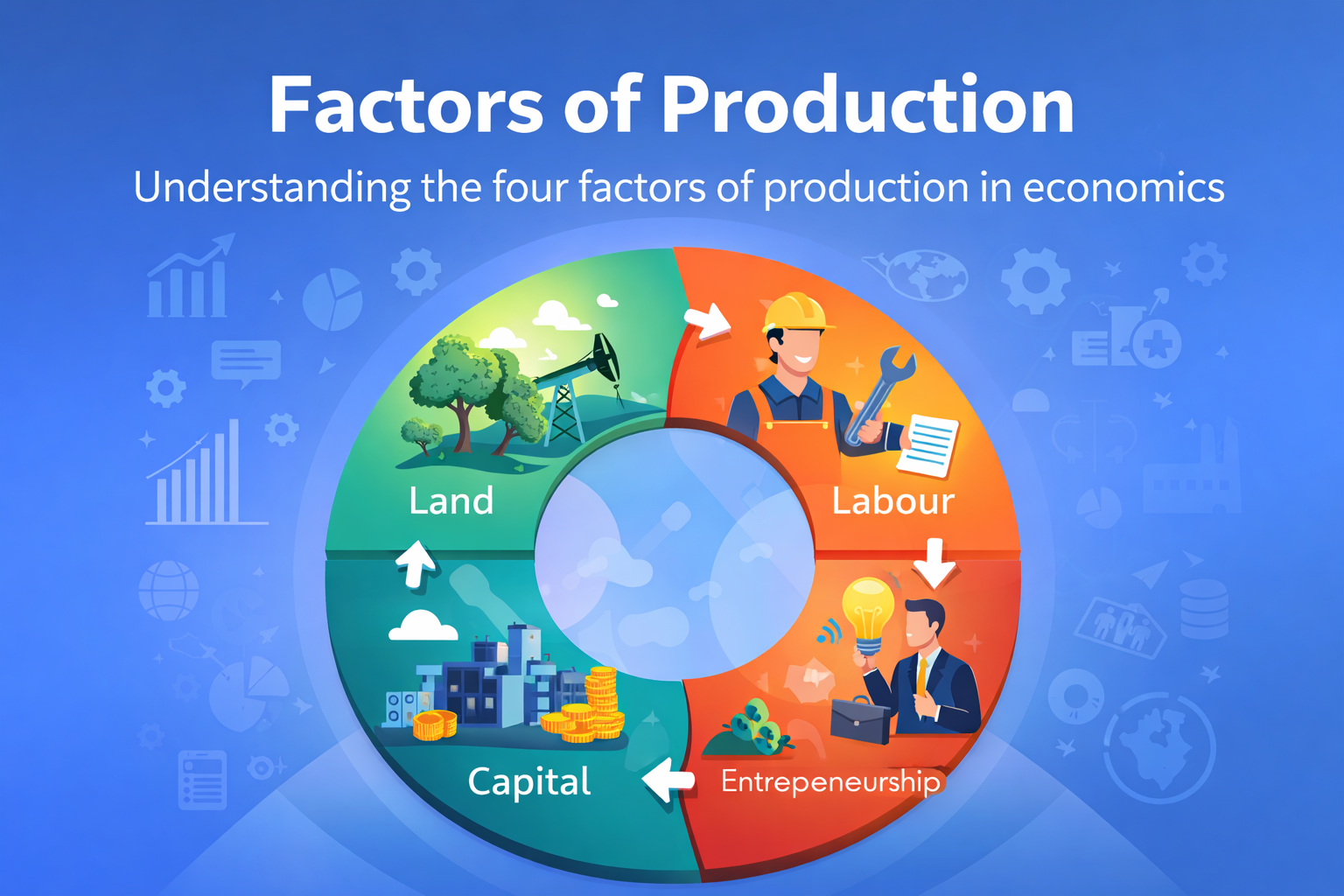

They are the resources required to create output. In factors of production in economics, these resources are traditionally grouped into four factors of production:

- Land

- Labour

- Capital

- Entrepreneurship

When people ask what are factors of production, they’re asking about these four categories that make production possible. Each factor plays a distinct role, earns a distinct type of income, and faces distinct limitations.

A quick way to remember:

- Land supplies natural resources.

- Labour supplies human effort and skills.

- Capital supplies tools and infrastructure.

- Entrepreneurship supplies coordination, innovation, and risk-taking.

Why Factors of Production Matter in Economics

The idea of factors of production helps explain major economic questions like:

- Why do workers earn wages?

- Why do owners of buildings earn rent?

- Why do lenders earn interest?

- Why do business owners earn profit?

- Why are some countries richer than others?

- What drives productivity and economic growth?

When you explain the factors of production, you’re really explaining how economies organize resources to produce value, and how income gets distributed among different contributors.

The Four Factors of Production in Economics

Let’s break down the four factors of production one by one, properly, with examples and the key economic logic.

1) Land as a Factor of Production

In everyday language, land means plots of soil. In factors of production in economics, land is broader. It includes all natural resources used in production.

What “Land” Includes

Land covers things like:

- Agricultural land (soil, fertility, water availability)

- Forests and timber

- Rivers, lakes, fisheries

- Minerals (iron, copper, bauxite)

- Fossil fuels (coal, oil, natural gas)

- Sunlight and wind (energy resources)

- Geographic location advantages (ports, trade routes)

- Natural ecosystems and biodiversity (increasingly important)

So when we ask again, what are the factors of production?, land is the part that nature provides without human creation.

Key Characteristics of Land

Land as a factor of production has some unique characteristics:

- **Fixed supply (limited availability)**In many cases, land is scarce. You can improve it, but you can’t easily increase total supply. This scarcity shapes prices and economic power.

- ImmobilityLand cannot be moved. Location matters. The same activity may be profitable in one location and impossible in another.

- Different qualityNot all land is equal. Fertile soil differs from rocky soil. A coal-rich region differs from a desert.

- Derived demandThe demand for land depends on demand for goods and services produced from it. More demand for wheat increases demand for farmland.

Income Earned by Land: Rent

In factors of production in economics, land earns rent.

Rent is the payment made for use of land or natural resources.

Important note: “rent” in economics is not only house rent. It includes payments for using any natural resource.

Real Examples of Land

- A farmer uses fertile soil and water to grow rice.

- A cement company uses limestone from quarries.

- A solar power plant uses sunlight and open area.

- A factory gains from being near highways and ports.

Land is often underestimated in modern conversations, but it quietly shapes costs, access, and long-term sustainability.

2) Labour as a Factor of Production

Labour means human effort used to produce goods and services. It includes both physical and mental work.

So if you’re asking what are factors of production, labour is the “human input” side: time, energy, skills, knowledge, and creativity applied to production.

What Labour Includes

Labour covers:

- Factory workers assembling products

- Teachers educating students

- Nurses providing care

- Engineers designing machines

- Drivers transporting goods

- Accountants managing finance

- Programmers writing code

- Managers coordinating teams

Labour is not only “hard work.” It includes skill, training, decision-making, and problem-solving.

Types of Labour

In factors of production in economics, labour can be categorized in useful ways:

- Skilled vs Unskilled Labour

- Skilled: surgeons, engineers, pilots

- Unskilled: basic manual workers without specialized training

- Physical vs Mental Labour

- Physical: construction, farming, logistics

- Mental: design, analysis, administration, research

- Direct vs Indirect Labour

- Direct: workers directly producing goods

- Indirect: staff supporting production (maintenance, HR, supervisors)

Productivity and Human Capital

Here’s the thing: labour becomes far more valuable when it’s productive. That’s where human capital comes in.

Human capital means education, health, training, and experience that make labour more effective. A well-trained worker often produces more output per hour than an untrained worker, even with the same machines.

So when we explain the factors of production, labour is not just “number of workers.” It’s “quality and productivity of workers.”

Income Earned by Labour: Wages

Labour earns wages (and salaries).

Wages represent payment for time and effort.

Wages depend on:

- Skills and scarcity of talent

- Productivity and output value

- Market demand for certain jobs

- Bargaining power and labour laws

- Technology changes (automation can shift demand)

Real Examples of Labour

- A chef turns raw ingredients into meals.

- A technician maintains machines to prevent downtime.

- A designer makes packaging more appealing and boosts sales.

- A call center team improves customer retention.

Labour is the most visible factor in daily life, because most people earn their income through it.

3) Capital as a Factor of Production

In common language, “capital” often means money. In factors of production in economics, capital means man-made tools and assets used to produce other goods and services.

So capital is not the final product. It is the equipment, infrastructure, and tools that help production happen efficiently.

What Capital Includes

Capital includes:

- Machines and equipment

- Tools and instruments

- Buildings and factories

- Roads, ports, warehouses

- Computers and servers

- Vehicles used in business

- Technology systems used in production

- Irrigation systems and farm machinery

Money is not capital by itself. Money becomes useful as capital when it is invested in productive assets.

Types of Capital

- Fixed CapitalUsed repeatedly over time:

- machines, buildings, vehicles

- Working CapitalUsed up in the production cycle:

- raw materials, fuel, packaging, inventory

- Physical vs Financial Capital

- Physical: machines, buildings

- Financial: funds that enable purchase of physical capital

Why Capital Matters So Much

Capital improves productivity. A worker using modern machinery can produce far more than a worker using bare hands.

This is one reason countries with better infrastructure and capital investment often have higher output per worker.

So if you revisit the question what are the factors of production, capital answers: “What do we use to make work more effective?”

Income Earned by Capital: Interest

Capital typically earns interest (or returns).

If someone invests in a factory, buys machines, or lends funds that become productive assets, they expect compensation. In economics, this compensation is generally represented as interest or returns on investment.

Real Examples of Capital

- A bakery’s oven and mixer are capital.

- A delivery company’s fleet of vans is capital.

- A hospital’s MRI machine is capital.

- A software company’s servers are capital.

Capital is the factor that often decides scale. With limited capital, production stays small. With sufficient capital, output can grow fast.

4) Entrepreneurship as a Factor of Production

Now we come to the most misunderstood part of the four factors of production: entrepreneurship.

Entrepreneurship is the ability to organize land, labour, and capital, make decisions, take risks, and create a functioning business that produces output.

If land is nature, labour is human effort, and capital is tools, then entrepreneurship is the “brain” that combines them into a productive system.

What Entrepreneurs Actually Do

Entrepreneurship includes:

- Identifying opportunities in the market

- Deciding what to produce

- Creating a business plan and strategy

- Hiring workers and building teams

- Raising funds and managing capital

- Choosing technology and production methods

- Marketing and building distribution

- Taking risks in uncertain markets

- Innovating products and processes

So when we explain the factors of production, entrepreneurship is the deciding factor that converts resources into results.

Risk and Uncertainty

A key feature of entrepreneurship is risk-bearing.

- Workers earn wages even if the business makes a loss.

- Landowners earn rent based on contracts.

- Capital providers may earn interest through structured returns.

- Entrepreneurs face uncertain profits and losses.

They take responsibility for outcomes. That’s why entrepreneurship is rewarded differently.

Income Earned by Entrepreneurship: Profit

Entrepreneurship earns profit.

Profit is not a guaranteed income. It is what remains after paying:

- wages to labour

- rent to land

- interest/returns to capital

- taxes and operational costs

Profit is the reward for:

- innovation

- decision-making

- coordination

- risk-taking

Real Examples of Entrepreneurship

- A founder sets up a dairy brand, sources milk, hires staff, buys equipment, and sells to retailers.

- A tech entrepreneur builds an app, funds servers, hires developers, and finds a monetization model.

- A small shop owner manages inventory, pricing, customer service, and competition daily.

Entrepreneurship is what turns “resources” into “a working production system.”

Factors of Production Working Together: A Simple Example

Let’s take a simple product: bread.

To produce bread:

- Land: wheat farms, water, land for bakery location

- Labour: farmers, mill workers, bakers, delivery staff

- Capital: tractors, mills, ovens, packaging machines, trucks

- Entrepreneurship: someone organizes supply, sets prices, ensures quality, sells bread, manages risks

This is why the concept of factors of production is so useful. It gives a complete picture of how production actually happens.

Factors of Production in Economics: The Reward System

A classic way to summarize factors of production in economics is by linking each factor with its income:

- Land → Rent

- Labour → Wages

- Capital → Interest

- Entrepreneurship → Profit

This reward system explains income distribution in an economy.

Are There Only Four Factors of Production?

Most textbooks use the four factors of production. But modern discussions sometimes add a fifth: technology or knowledge.

Here’s the clean way to see it:

- Technology often acts like an improvement in capital (better machines, better systems).

- Knowledge often acts like improved labour (higher human capital).

- Innovation is often driven by entrepreneurship.

So yes, you’ll hear expansions. But the standard answer to what are the factors of production remains the classical four, because they cover the whole production process in a stable framework.

The Role of Technology Within the Four Factors

Even without labeling technology as a separate factor, it deeply affects each one:

Technology and Land

- Precision agriculture increases output from the same land.

- Water-saving irrigation improves efficiency.

Technology and Labour

- Workers become more productive with software, automation, and training.

- New jobs emerge, old jobs decline.

Technology and Capital

- Machines become smarter and faster.

- Production becomes scalable with digital infrastructure.

Technology and Entrepreneurship

- Entrepreneurs can reach global markets through digital platforms.

- Data improves decision-making, but also increases competition.

So while the definition stays consistent, real-world production keeps evolving.

Factor Intensity: Which Factor Dominates?

Some industries rely heavily on one factor more than others.

Land-Intensive Industries

- Agriculture

- Mining

- Fisheries

Labour-Intensive Industries

- Handicrafts

- Hospitality

- Many services

- Small-scale manufacturing

Capital-Intensive Industries

- Automobile manufacturing

- Oil refining

- Telecom infrastructure

- Large hospitals

Entrepreneurship-Intensive Markets

In reality, entrepreneurship matters everywhere, but it becomes especially visible in:

- Startups

- Innovative consumer brands

- High-competition markets where strategy matters as much as resources

Understanding factor intensity helps explain cost structures and competitive advantage.

Productivity: The Big Goal of Combining Factors

Production is not only about having more resources. It’s also about using them well.

Productivity means output per unit of input. For example:

- Output per worker hour (labour productivity)

- Output per machine hour

- Output per acre of land

When productivity rises, an economy can produce more without necessarily increasing inputs.

This is one of the deepest implications of factors of production in economics: growth can come from better use of factors, not just more factors.

Scarcity and Choice: The Economic Reality Behind Factors

Here’s the thing: every factor is scarce in some way.

- Land is limited and unevenly distributed.

- Labour is limited by population, skills, and health.

- Capital is limited by savings and investment capacity.

- Entrepreneurship is limited by risk appetite, capability, and environment.

Scarcity forces choices. Choices create opportunity costs. That’s why factors of production sit at the center of economic thinking.

Mobility of Factors: Can They Move Easily?

Another important idea in factors of production is mobility, how easily a factor shifts from one use to another.

Land Mobility

Low mobility. Location is fixed.

Labour Mobility

Moderate mobility. People can change jobs, but moving cities or reskilling takes time and money.

Capital Mobility

Often higher mobility, especially financial capital. But physical capital like factories is less mobile.

Entrepreneurship Mobility

Depends on policy, opportunity, access to finance, and ecosystem support.

Mobility affects development. If factors can move to their best use, productivity and growth rise faster.

Factors of Production and Economic Development

When economists compare countries, they often ask:

- Does the country have enough productive land and resources?

- Is the labour force skilled and healthy?

- Is there enough capital investment?

- Does the environment support entrepreneurs?

Development often accelerates when:

- education improves (labour quality rises)

- infrastructure expands (capital deepens)

- institutions support business (entrepreneurship strengthens)

- resources are used sustainably (land remains productive)

This is why factors of production in economics is a foundational framework for understanding national growth.

Sustainability: Using Factors Without Destroying Them

Modern economics cannot ignore sustainability, especially for land and resources.

- Overuse of soil reduces fertility.

- Pollution reduces usable water.

- Over-mining creates environmental costs that future generations pay.

- Unhealthy labour conditions reduce long-term productivity.

Good economies don’t just “use factors.” They manage them wisely so production can continue long-term.

Real-World Case Study: A Small Clothing Brand

Let’s make this practical. Imagine a small clothing brand producing cotton t-shirts.

Land

- Cotton farms

- Water resources

- Factory location and logistics routes

Labour

- Farmers and pickers

- Textile workers

- Tailors, quality inspectors

- Sales and support teams

Capital

- Spinning machines

- Stitching machines

- Dyeing equipment

- Warehouse and delivery vehicles

Entrepreneurship

- Brand owner chooses designs, pricing, sourcing

- Manages suppliers, costs, and marketing

- Takes risk on inventory and demand

This is exactly how the four factors of production show up in real businesses.

Common Confusions About Factors of Production

Confusion 1: “Capital means money”

Not in the strict economic sense. Money is a means to acquire capital, but capital is the productive asset itself.

Confusion 2: “Entrepreneurs are the same as capitalists”

Not always. A person can be an entrepreneur without owning much capital (they may raise funds). A person can own capital without running a business.

Confusion 3: “Land means only farmland”

Land includes all natural resources used in production, including energy sources and minerals.

When people ask explain the factors of production, clearing these confusions is often the biggest step toward real understanding.

Factors of Production and the Modern Service Economy

A common question is: do factors of production still matter when economies shift toward services?

Yes, absolutely.

A service business still needs:

- Land: office space, location, internet infrastructure footprint

- Labour: employees and skills

- Capital: computers, software, systems, equipment

- Entrepreneurship: strategy, customer acquisition, innovation

Even digital products rely on data centers, electricity, skilled labour, and entrepreneurial direction.

So if anyone asks what are the factors of production in the modern economy, the answer stays the same, only the examples change.

Summary: What Are the Factors of Production?

Let’s tie it together clearly.

Factors of production are the inputs needed to create goods and services. In factors of production in economics, the standard framework is the four factors of production:

- Land (natural resources)

- Labour (human effort and skills)

- Capital (man-made tools and productive assets)

- Entrepreneurship (organization, innovation, and risk-bearing)

Understanding what are the factors of production helps you understand how production happens, how income is distributed, and why growth differs across industries and countries.

FAQs (7)

1) What are the factors of production?

What are the factors of production? They are the inputs used to produce goods and services. The standard four factors of production are land, labour, capital, and entrepreneurship.

2) What are factors of production in economics used for?

Factors of production in economics are used to explain how goods and services are produced, how costs are formed, how incomes are distributed (wages, rent, interest, profit), and what drives productivity and growth.

3) Why are there four factors of production?

The four factors of production cover the full production process: nature’s resources (land), human effort (labour), tools and infrastructure (capital), and decision-making plus risk-taking (entrepreneurship). Together, they explain how output is created.

4) Is technology a factor of production?

Many modern discussions treat technology as a separate factor, but traditionally it’s considered part of capital (better tools) and labour (better skills), and often driven by entrepreneurship (innovation). The classical model still focuses on the four factors of production.

5) What income does each factor of production earn?

In factors of production in economics:

- Land earns rent

- Labour earns wages

- Capital earns interest/returns

- Entrepreneurship earns profit

6) What is the most important factor of production?

There isn’t one universal “most important” factor. It depends on the industry and context. Agriculture relies heavily on land, services rely heavily on labour, manufacturing can be capital-intensive, and competitive markets strongly depend on entrepreneurship.

7) How do factors of production affect economic growth?

Growth happens when a country increases the quantity or quality of its factors of production (more skilled labour, more capital investment, better resource use) and when productivity improves through smarter combination of land, labour, capital, and entrepreneurship.