India's personal income tax landscape underwent one of its most significant transformations in recent memory when the government made the new tax regime the default option starting FY 2023–24. Since then, millions of salaried employees, self-employed professionals, and business owners have had to make a critical decision: stick with the familiar old regime or embrace the new one?

If you're still on the fence — or simply want to understand exactly what the new tax regime slabs mean for your take-home pay — this guide is for you. We'll walk through everything: the revised slabs, the rebates, what deductions you lose, when the new regime wins, and the scenarios where holding onto the old regime still makes sense.

What Is the New Tax Regime?

The new tax regime was first introduced in the Union Budget of 2020 as an optional alternative to the existing (old) tax structure. The idea was straightforward: offer taxpayers lower tax rates in exchange for giving up the maze of exemptions and deductions that had made Indian income tax filing notoriously complex.

For years, the new regime remained a niche choice — primarily because the rate advantage wasn't compelling enough to justify losing deductions like HRA, Section 80C, and home loan interest. That changed dramatically with the Union Budget 2023, when Finance Minister Nirmala Sitharaman announced sweeping revisions that made the new tax regime not just competitive, but genuinely attractive for a large segment of taxpayers.

The government's intent is clear: simplify compliance, reduce paperwork, and eventually phase out the patchwork of exemptions that complicate India's tax code. The new regime is the vehicle for that vision.

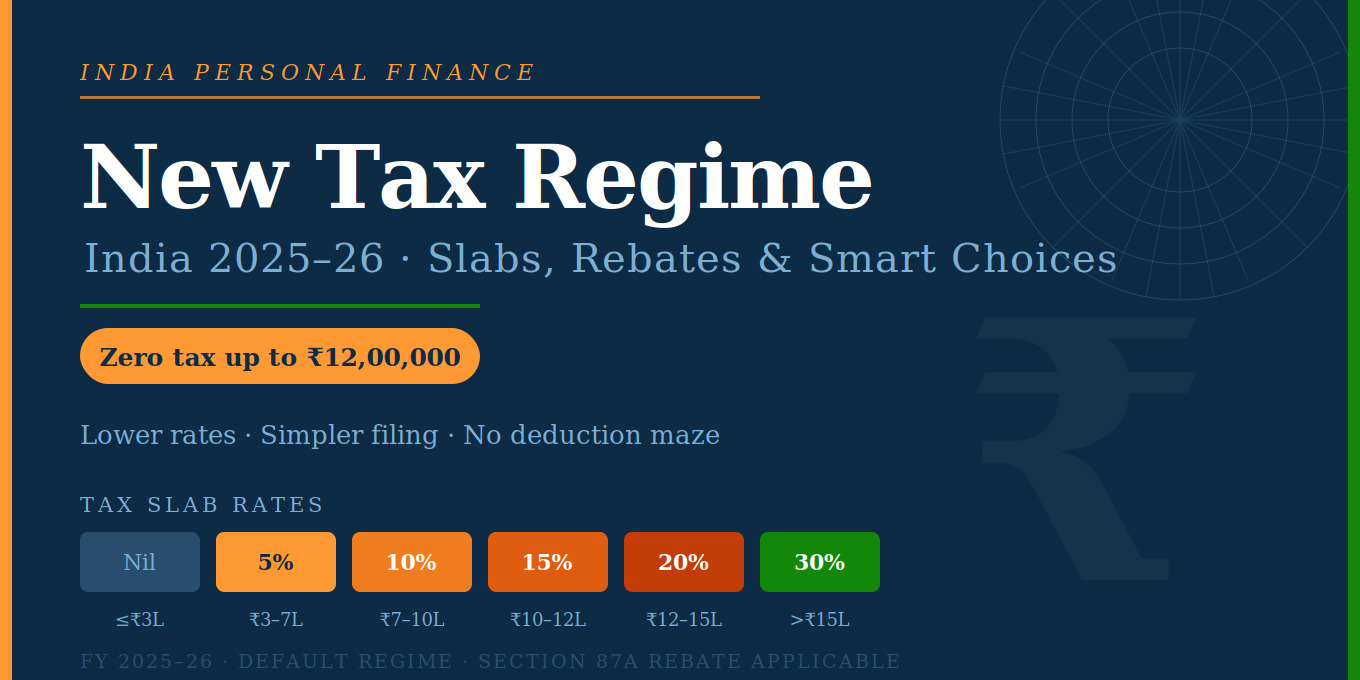

New Tax Regime Slabs: FY 2024–25 and FY 2025–26

The most important thing to understand about the new tax regime is its slab structure — lower headline rates applied to wider income brackets.

Here are the new tax regime slabs currently in effect:

Annual Income (₹) | Tax Rate |

|---|---|

Up to ₹3,00,000 | Nil |

₹3,00,001 – ₹7,00,000 | 5% |

₹7,00,001 – ₹10,00,000 | 10% |

₹10,00,001 – ₹12,00,000 | 15% |

₹12,00,001 – ₹15,00,000 | 20% |

Above ₹15,00,000 | 30% |

Note: A 4% Health & Education Cess applies on the total tax payable across all slabs.

The ₹7 Lakh Rebate — A Game-Changer

One of the most consequential features of the revised new tax regime is the enhanced rebate under Section 87A. If your total taxable income does not exceed ₹7,00,000, you pay zero tax — even though the slab technically shows a 5% rate between ₹3 lakh and ₹7 lakh.

This effectively means individuals earning up to ₹7 lakh annually have no income tax liability whatsoever under the new regime, making it highly attractive for middle-income earners.

For FY 2025–26 (announced in Budget 2025), this threshold was further raised to ₹12,00,000, meaning taxpayers earning up to ₹12 lakh will pay zero tax under the new tax regime, subject to the rebate conditions. With the standard deduction of ₹75,000, salaried individuals effectively receive this benefit up to a gross salary of ₹12.75 lakh.

This is a landmark shift. It means the new tax regime now offers complete tax relief for a much larger portion of the working population than ever before.

Standard Deduction Under the New Tax Regime

Until FY 2022–23, the standard deduction of ₹50,000 was available only under the old regime. The Budget 2023 extended it to the new tax regime as well — and Budget 2024 increased it to ₹75,000 for salaried employees and pensioners.

This single change significantly improved the effective advantage of the new regime for salaried taxpayers. At higher income levels, ₹75,000 off the top before calculating tax isn't trivial — it can mean the difference of thousands of rupees annually.

What You Give Up: Deductions Not Available Under the New Regime

The trade-off is real. The new tax regime does not permit most of the popular deductions and exemptions available under the old regime. Before making your choice, understand what's off the table:

Deductions and exemptions NOT available under the new tax regime:

- Section 80C — investments in PPF, ELSS, life insurance premiums, NSC, home loan principal repayment (up to ₹1.5 lakh)

- Section 80D — health insurance premiums (self, family, parents)

- Section 80E — interest on education loans

- Section 80G — charitable donations

- Section 80TTA/80TTB — interest on savings accounts / senior citizen interest income

- HRA (House Rent Allowance) — a major component for urban salaried professionals

- LTA (Leave Travel Allowance)

- Section 24(b) — interest on housing loan for self-occupied property (up to ₹2 lakh)

- Professional Tax deduction

- Most allowances beyond the standard deduction

What IS available under the new regime:

- Standard deduction of ₹75,000 (salaried/pensioners)

- Employer's contribution to NPS (Section 80CCD(2)) — this is a significant retained benefit

- Agniveer Corpus Fund deduction (Section 80CCH)

- Gratuity and leave encashment exemptions

- Conveyance allowance for disabled employees

- Deduction on family pension

Who Benefits Most from the New Tax Regime?

The new tax regime isn't universally superior — but it clearly benefits specific profiles more than others.

1. Young Professionals and Early-Career Earners

If you're early in your career, your income is moderate and you likely haven't yet accumulated significant 80C investments, home loans, or other deduction-generating commitments. For someone earning between ₹7 lakh and ₹12 lakh with minimal investments, the new tax regime slabs deliver materially lower taxes without requiring any planning effort.

2. Salaried Employees in the ₹12–15 Lakh Range

With the standard deduction now at ₹75,000 and the zero-tax rebate applicable up to ₹12 lakh, a salaried employee earning ₹12.75 lakh gross pays effectively nothing in income tax under the new regime — a powerful incentive.

3. Those with Employer NPS Contributions

Section 80CCD(2) — the employer's NPS contribution deduction — is one of the few significant deductions retained in the new tax regime. If your employer contributes to your NPS (up to 10% of basic salary for private sector, 14% for government employees), you can claim this deduction even within the new framework, making the regime even more attractive.

4. Taxpayers Who Dislike the Compliance Burden

Let's be honest: one underappreciated benefit of the new tax regime is simplicity. No need to collect rent receipts, maintain investment proofs, or time your Section 80C investments before year-end. For many people — especially business owners filing complex returns — this reduction in administrative overhead is a genuine quality-of-life improvement.

When the Old Regime May Still Win

Despite the government's push toward the new tax regime, there are valid scenarios where the old regime delivers better outcomes.

High HRA Claims in Metro Cities

If you live in Mumbai, Delhi, Bengaluru, or another metro city and pay substantial rent, HRA exemptions can be enormous — sometimes ₹2–4 lakh or more annually. This benefit disappears under the new regime. For a taxpayer in the 30% bracket with large HRA, old regime savings can be significant.

Large Home Loan Interest Deductions

Section 24(b) allows up to ₹2 lakh deduction on interest paid for a self-occupied property. For someone who recently bought a home and is servicing a large EMI, losing this deduction under the new tax regime can result in higher overall tax.

Maximum 80C Utilization Combined with 80D

If you're already maximizing your ₹1.5 lakh Section 80C limit (through EPF, PPF, ELSS, insurance) and also claiming ₹25,000–₹50,000 under 80D for health insurance, these deductions combined create a buffer that sometimes outweighs the lower rate advantage of the new regime — particularly for taxpayers in the ₹15–25 lakh income range.

Senior Citizens with Significant Interest Income

Senior citizens earning higher interest income from FDs and savings accounts benefit from the ₹50,000 deduction under Section 80TTB in the old regime. Depending on the amount, this may tip the math in favour of the old structure.

Switching Between Regimes: The Rules

One frequently misunderstood aspect of the new tax regime is the flexibility — or lack thereof — to switch between the two options.

Salaried individuals and pensioners can switch between the old and new tax regime every year. Each year, you inform your employer of your preferred regime for TDS purposes, and you can choose differently when filing your ITR.

Business owners and those with business income (non-salary) have less flexibility. If you opt out of the new tax regime, you can return to it only once in your lifetime. This makes the decision more consequential for entrepreneurs and self-employed professionals.

How to Calculate Your Tax Under the New Regime: A Practical Example

Let's take a concrete example to make the new tax regime slabs tangible.

Ravi, a software engineer in Pune, earns ₹14,00,000 gross salary annually.

Under the new tax regime:

- Gross Salary: ₹14,00,000

- Less: Standard Deduction: ₹75,000

- Net Taxable Income: ₹13,25,000

Tax calculation:

- Up to ₹3 lakh: Nil

- ₹3–7 lakh @ 5%: ₹20,000

- ₹7–10 lakh @ 10%: ₹30,000

- ₹10–12 lakh @ 15%: ₹30,000

- ₹12–13.25 lakh @ 20%: ₹25,000

- Total Tax: ₹1,05,000

- Add 4% Cess: ₹4,200

- Total Tax Payable: ₹1,09,200

Under the old regime (assuming ₹1.5L 80C + ₹25K 80D + ₹60K HRA):

- Gross: ₹14,00,000

- Standard Deduction: ₹50,000

- HRA: ₹60,000

- 80C: ₹1,50,000

- 80D: ₹25,000

- Net Taxable Income: ₹11,15,000

Tax under old slabs: approximately ₹1,62,500 before cess.

In this case, the new tax regime saves Ravi approximately ₹57,000 — a clear win. The math shifts when deductions are larger, but for average salaried professionals with moderate investments, the new regime frequently comes out ahead.

New Tax Regime for Businesses and Self-Employed Professionals

The new tax regime applies equally to individuals with business or professional income. The core new tax regime slabs are identical — but there are some important nuances:

- Presumptive taxation under Sections 44AD, 44ADA, and 44AE is compatible with the new regime

- Business expenses remain deductible (since these are not "deductions" but expense recognition)

- Depreciation under Section 32 is not available under the new regime for certain assets

- Carry forward of losses under certain heads may be restricted when switching regimes

For freelancers and consultants, the new regime can be compelling if their actual deductible expenses are captured through presumptive taxation, and they don't rely heavily on the HRA or investment-linked deductions of the old framework.

The Bigger Picture: Why India Is Moving in This Direction

The shift toward the new tax regime reflects broader policy goals. The government wants to:

- Simplify the tax code — fewer exemptions mean simpler filing, lower compliance costs, and reduced scope for misreporting.

- Encourage consumption over forced savings — the old regime's deductions effectively nudged people to invest in specific instruments. The new regime gives individuals freedom to allocate their money as they see fit.

- Widen the tax base — simpler filing and lower rates may bring more individuals into voluntary compliance.

- Align with global norms — most advanced economies use straightforward progressive slabs without elaborate exemption ecosystems.

The trajectory is clear: the old regime is being kept alive for now, but the government's intent is to eventually make the new tax regime the sole framework — likely after ensuring the majority of taxpayers are financially better off under it.

Common Mistakes to Avoid

1. Not running the comparison every year Your financial situation changes. A year you take a home loan or make large 80C investments may favour the old regime even if previous years didn't. Run the numbers annually.

2. Forgetting employer NPS benefit Many employees don't realise that their employer's NPS contribution is still deductible under the new tax regime. If your employer offers this, factor it in — it can swing the comparison.

3. Assuming the new regime always wins above ₹12 lakh This is a common misconception. At higher income levels with significant deductions, the old regime can still deliver lower tax. The break-even point depends on the total value of your eligible deductions.

4. Informing your employer too late For accurate TDS deduction, inform your employer of your preferred regime at the start of the financial year. Changing midway causes complications, though it can be rectified at the time of ITR filing.

Quick Decision Framework

Ask yourself these three questions:

Q1: Is your gross annual income below ₹12.75 lakh? → Yes: The new tax regime almost certainly wins. Zero tax liability with the rebate and standard deduction.

Q2: Do your total eligible deductions (HRA + 80C + 80D + home loan interest) exceed ₹4–5 lakh? → Yes: Run a detailed comparison. The old regime may still be competitive at this level of deductions.

Q3: Do you value simplicity and hate year-end investment scrambles? → Yes: The new tax regime offers real lifestyle value beyond just the numbers — no investment pressure, no paperwork marathons.

Conclusion: The New Tax Regime Is the Future

The new tax regime has matured considerably since its lukewarm reception in 2020. With revised new tax regime slabs, an enhanced standard deduction, and a dramatically expanded zero-tax rebate, it now genuinely serves the majority of Indian taxpayers — especially salaried professionals, young earners, and those without large deduction portfolios.

That said, it's not a one-size-fits-all solution. If you have a home loan, claim large HRA, and consistently maximise Section 80C, the old regime may still save you money. The key is doing the math — ideally with a CA or a reliable tax calculator — rather than defaulting to either option without analysis.

What's certain is the direction of travel. India's tax policy is on a deliberate path toward simplification, and the new tax regime is at the center of that journey. Understanding its slabs, its benefits, and its trade-offs isn't just good financial hygiene — it's increasingly essential knowledge for every earning Indian.

Disclaimer: Tax laws are subject to change. Always consult a qualified chartered accountant or tax professional for advice specific to your financial situation. This article reflects rules as of FY 2025–26 and may not account for subsequent amendments.

FAQ:

1. What is the new tax regime in India?

The new tax regime is a simplified income tax structure introduced in 2020, offering lower slab rates in exchange for foregoing most deductions and exemptions like 80C, HRA, and home loan interest.

2. What are the new tax regime slabs for FY 2025–26?

The new tax regime slabs are: Nil up to ₹3L, 5% for ₹3–7L, 10% for ₹7–10L, 15% for ₹10–12L, 20% for ₹12–15L, and 30% above ₹15L. A 4% cess applies on total tax.

3. Who does not need to pay any tax under the new tax regime?

Individuals with a taxable income up to ₹12,00,000 pay zero tax under the new tax regime due to the Section 87A rebate. Salaried individuals with gross income up to ₹12,75,000 are also covered, thanks to the ₹75,000 standard deduction.

4. Is the new tax regime mandatory for salaried employees?

No, but it is the default regime from FY 2023–24 onwards. Salaried employees can opt for the old regime every financial year by informing their employer. The choice can be revised at the time of filing the ITR.

5. What deductions are allowed under the new tax regime?

The new tax regime allows the standard deduction of ₹75,000 for salaried individuals and the employer's NPS contribution under Section 80CCD(2). Most other deductions — including 80C, 80D, HRA, and home loan interest — are not available.

6. Can I switch between old and new tax regime every year?

Salaried individuals and pensioners can switch between regimes every year. However, taxpayers with business or professional income can opt out of the new tax regime only once, after which they cannot return to it.

7. Is the new tax regime better than the old regime?

It depends on your deductions. For most salaried individuals earning up to ₹12–15L with moderate investments, the new tax regime is better. If you have large HRA claims, a home loan, or maximise 80C and 80D, the old regime may still save more tax.

8. What is the standard deduction under the new tax regime?

The standard deduction under the new tax regime is ₹75,000 for FY 2025–26, applicable to salaried employees and pensioners. This was increased from ₹50,000 in the Union Budget 2024.